The Story of Digital Assets May Be Just Beginning

The war in the Middle East, which has shaken global markets, has had many different consequences. Rising energy costs, their potential impact on global economic growth in the coming period, and their geographical implications are causing the cards to be reshuffled and the rules of the game to change.

These chaotic and historic developments also have implications for digital assets. Bitcoin, the largest cryptocurrency by market capitalization, has attracted attention with the different roles it has assumed since the first days of the war. During the days when the risk aversion trend resulting from the war was most pronounced, Bitcoin acted as an “escape ramp,” isolated from traditional financial instruments. We have also seen it priced at times as a high-beta, risky asset during the ongoing war. However, while one of the most disruptive experiences in history for global markets is unfolding, it would not be wrong to say that Bitcoin is (for now) successfully navigating this significant test with minor scratches. According to CME Group data and expectations, which we will examine in detail, there are some important clues regarding this. In other words, while Bitcoin’s adoption process by traditional markets continues, there is no sign that its appeal is diminishing.

The Impact of Regulatory Bodies

The Securities and Exchange Commission (SEC) in the United States, which has the world’s largest economy, has taken important steps regarding digital assets in recent times. Regulatory support, such as the adoption of General Listing Standards (GLS) and the Digital Asset Market Clarity Act (CLARITY), has made it easier for investors to invest in digital assets through Exchange Traded Funds (ETFs). Subsequently, the traditional finance (TradFi) sector’s interest in digital currencies has been far from negligible.

Delays in the adoption of these regulations and laws, uncertainties surrounding certain dynamics unique to digital assets, and factors deeply affecting global markets (Trump’s tariffs, concerns about AI companies being overvalued, questions about the independence of the US Federal Reserve (FED), geopolitical developments-wars) have not completely dampened investor appetite in the ETF sector, despite occasionally negatively affecting fund flows. In fact, despite a $5 billion fund outflow in the last quarter of last year, a staggering $47.2 billion was raised for the entire year. Meanwhile, on Wall Street, there is talk that the TradFi sector’s interest in digital currencies remains intact and that new institutions will also enter this market. It is said that this could help double the amount of money entering ETFs by 2026. By 2027, with more institutions and state funds entering this space, this “increase” is projected to rise to 1.5 to 2 times its current level.

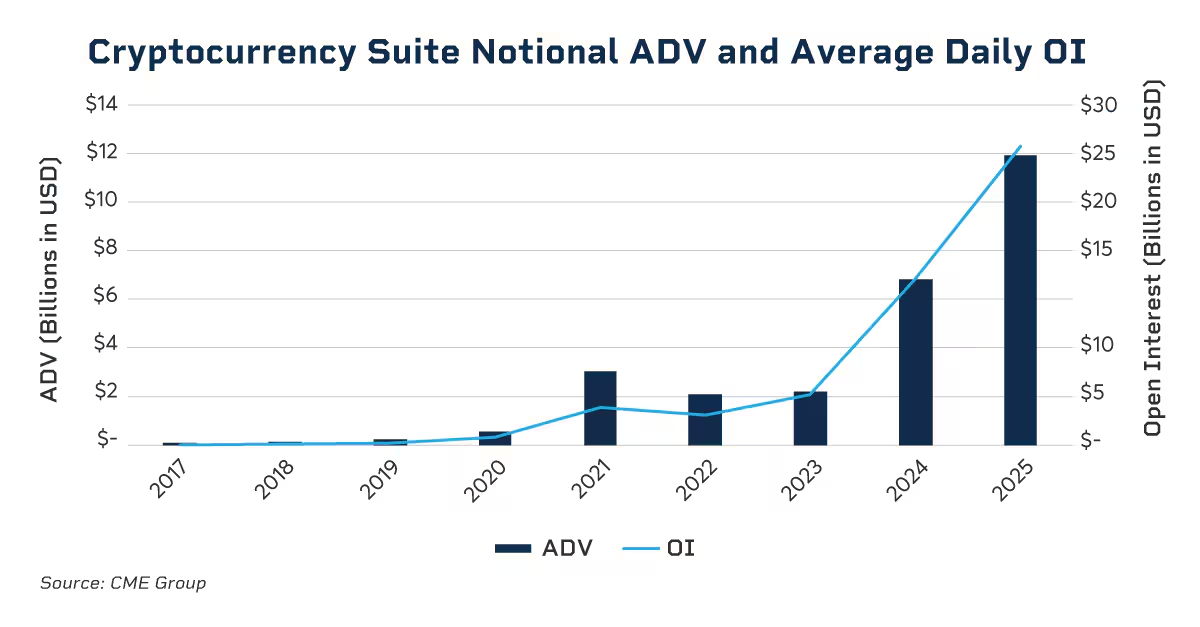

In fact, it is worth noting that such a fund inflow has been achieved despite the losses that followed Bitcoin’s historic peak at $126,000. The acceleration of institutional units such as banks and asset managers with the adoption of GLS also played a significant role in this. The significant easing of ETF listings with GLS has also created a wave of applications for popular altcoins such as Doge, Cardano, and Polkadot. This momentum has also reflected in the crypto derivatives space. CME Group launched Cardano, Chainlink, and Stellar futures, and the total notional volume showed a 75% increase in 2025 compared to 2024.

Prior to GLS, crypto ETFs were treated as “special cases” requiring lengthy and cumbersome applications subject to long delays. Under the new rules, if a crypto asset meets certain predefined criteria, the exchange can list it within five days without SEC approval.

Some of the legal criteria introduced by GLS include:

A crypto asset must:

- Has been traded as a futures contract for at least six months,

- Has an average liquidity of at least $700 million over a 12-month period,

- Is a member of the Intermarket Surveillance Group (ISG), which prevents fraud,

it can qualify for listing status. Thus, GLS has encouraged giants like Morgan Stanley and Goldman Sachs to launch their own crypto ETFs. It has also facilitated the emergence of basket ETFs containing various coins.

Another financial giant, Bank of America, allowing its investment advisors to recommend spot Bitcoin ETFs is a result of these regulations. Furthermore, Morgan Stanley, Fidelity, JP Morgan, and Wells Fargo have begun advising their clients to hold between 1% and 4% of their total assets in cryptocurrencies through similar steps.

The Future of CLARITY

The CLARITY Act, expected to be approved by Congress in the first half of this year, is at the center of attention for digital asset investors. Under this law, digital assets will be classified as “Digital Commodities” under the Commodity Futures Trading Commission (CFTC) rather than “securities” under the SEC’s authority. This means that fund issuers will not have to worry about being sued for holding “unregistered securities.” CLARITY also envisions ETFs being treated like stablecoins and enabling 24/7 real-time trading. With banks beginning to act as custodians, it is anticipated that trading, research, and advisory arms will also support this initiative, further deepening its adoption.

Conclusion

Last year, sovereign wealth funds such as Qatar’s QIA, Norway’s NBIM, and Abu Dhabi’s ADIA/Mubadala directly purchased Bitcoin. Additionally, the ease of listing ETFs based on digital assets can be seen as a factor encouraging institutions like Bank of America, which employs over fifteen thousand investment advisors, to enter the competition to gain a share of the market. The trend of companies positioning themselves as Bitcoin treasury companies, such as MicroStrategy, and the aforementioned sovereign wealth funds purchasing Bitcoin is expected to continue for the next 1-2 years. With new funds expected to continue entering ETFs, we may be experiencing a period where the story of digital assets is perhaps just beginning. Price fluctuations may vary depending on market conditions; they may fall or rise. However, the advantages of being a brand-new financial instrument that is the focus of investor interest, even institutional investors, seem likely to be discussed more extensively in the digital asset world.