Market Compass

Bitcoin Against Geopolitical Developments?

The war launched by the US and Israel against Iran on Friday shook global markets. While Bitcoin demonstrated a relatively strong pricing model amid this turmoil, the macroeconomic data we expected to discuss this week and expectations regarding the US Federal Reserve’s (FED) next interest rate cut, which could shape the market, have been put on hold.

Iran will remain on investors’ agenda for some time. We will continue to monitor how the situation evolves and how the scale of the war changes. According to President Trump, turmoil in the Middle East will continue for another 4-5 weeks. Iran, meanwhile, is not currently keen on coming to the table.

Beyond the geopolitical agenda, we will continue to monitor data coming out of the US throughout this week. Bitcoin’s solid performance will be tested by macro dynamics this time, and we will continue to monitor the potential impact of these developments.

March 6 – Critical U.S. Employment Data and Potential Impact on Bitcoin

The first critical macro indicators of March will be the U.S. labor market statistics. On March 6, we will receive employment data for February, with the Nonfarm Payrolls (NFP) being the focal point among the data sets that will provide valuable information about the Federal Reserve’s (FED) next interest rate move. The FED’s policy rate path, which will also determine liquidity conditions for the rest of the year, will be important for Bitcoin investors.

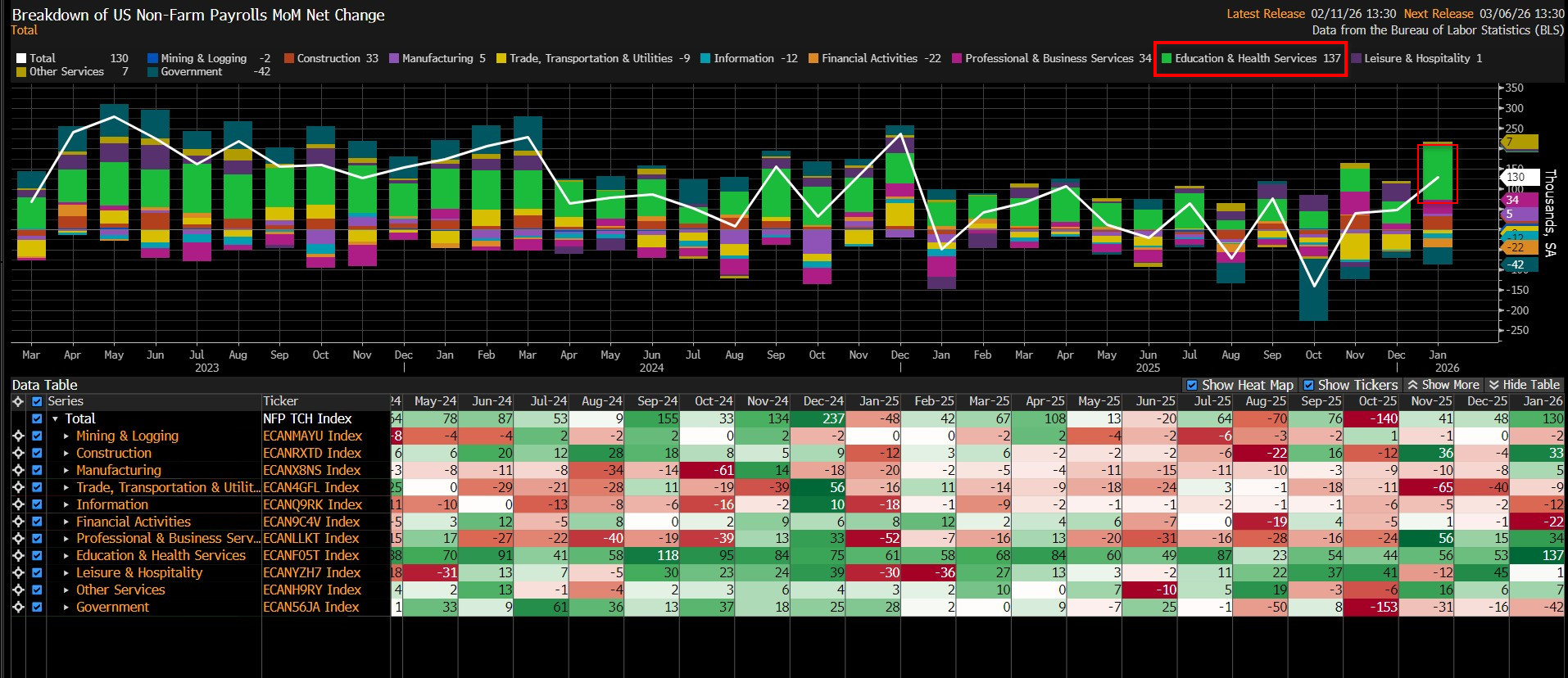

Over the past year, the NFP, which had been sending negative signals about the health of the US economy, showed that the country’s economy created 130,000 new jobs in non-farm sectors in January, indicating an increase well above forecasts (around 68,000). This picture revealed that the job market in the world’s largest economy was not as bad as previously thought. The sector that contributed most to employment in the relevant month was education and health services. The new NFP for February, to be announced on March 6, will shed light on the Federal Open Market Committee’s (FOMC) interest rate reduction path in the coming period.

U.S. NFP Data

Source: Bloomberg

Given the high market sensitivity to NFP data, our forecast is that the U.S. economy may have seen nonfarm payroll growth in February slightly above market expectations (according to the Bloomberg survey at the time of writing this report), but below the previous figure, and even below 100,000.

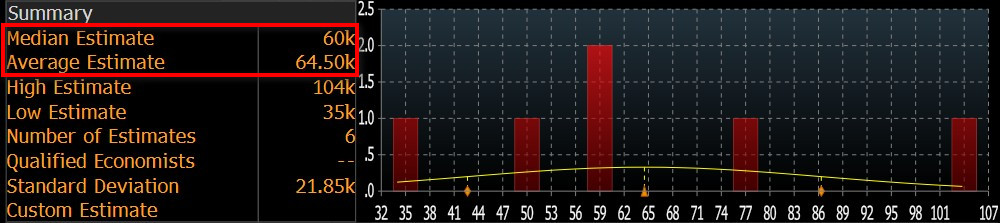

At the time of writing, although the number of forecasts entered is low, we see that the consensus (median forecast) in the Bloomberg survey is around 60,000, which is more pessimistic than our forecast model (this expectation figure may change later with new forecasts and new surveys, and most likely will change. However, it is still important to see the approximate analyst forecasts and understand market expectations. It would be beneficial to closely follow Darkex’s weekly newsletters for current forecasts). The average of the forecasts is around 64,000.

Source: Bloomberg

We believe that if February’s NFP data falls below expectations, it could strengthen expectations that the Fed may be more aggressive in lowering interest rates, thereby increasing risk appetite and having a positive impact on financial instruments, including digital assets. We believe that data above expectations could have the opposite effect.

Other Key Macroeconomic Indicators and Developments

March 2 – U.S. ISM Manufacturing PMI; The Purchasing Managers’ Index (PMI) is a diffusion index based on surveyed purchasing managers in the manufacturing industry. Conducted by The Institute for Supply Management (ISM), this survey of approximately 300 purchasing managers asks respondents to assess the relative level of business conditions, including employment, production, new orders, prices, supplier deliveries, and inventories. It is usually published monthly on the first business day after the end of the month, with a score above 50.0 indicating that the sector is expanding and below 50.0 indicating contraction. In general, a lower-than-expected ISM Manufacturing PMI is expected to have a positive impact on digital assets by pricing in expectations regarding the monetary policy course of the US Federal Reserve (FED). However, in some cases, it may also lead to pricing based on the strength of the economy. In this case, figures above expectations have a positive effect on digital assets.

March 4 – U.S. ADP Non-Farm Employment Change; shows the estimated change in the number of people employed in the previous month, excluding the agricultural sector and government, by the U.S. Bureau of Labor Statistics ( ). It analyzes payroll data from more than 25 million workers to obtain estimates of employment growth by Automatic Data Processing, Inc (ADP). It usually gives a hint of employment growth 2 days before the employment data released by the government. Typically, lower-than-expected ADP data has a positive impact on digital assets.

March 4 – U.S. ISM Services PMI; The Purchasing Managers’ Index (PMI) is a diffusion index based on surveyed purchasing managers excluding the manufacturing industry. Conducted by The Institute for Supply Management (ISM), this survey of approximately 300 purchasing managers asks respondents to assess the relative level of business conditions, including employment, production, new orders, prices, supplier deliveries, and inventories. It is usually published monthly on the third business day after the end of the month, with a score above 50.0 indicating that the sector is expanding and below 50.0 indicating contraction. In general, a lower-than-expected ISM Services PMI is expected to have a positive impact on digital assets by pricing in expectations regarding the monetary policy course of the US Federal Reserve (FED). However, in some cases, it may also lead to pricing based on the strength of the economy. In this case, figures above expectations have a positive effect on digital assets.

March 5 – U.S. Initial Jobless Claims; This shows the number of people who filed for unemployment insurance for the first time during the previous week and is published weekly, usually on the first Thursday after the week ends. Although it is a lagging indicator, the number of unemployed is considered an indicator of overall economic health because consumer spending is highly correlated with labor market conditions. Market impact can vary from week to week, and market participants tend to focus more on this data when they are more sensitive to recent developments or when macro indicators related to the labor market are at extreme levels.

March 6 – U.S. Retail Sales Data; It is an important measure of consumer spending, which accounts for a large part of overall economic activity. It shows the change in the total value of retail-level sales and is published monthly, about 16 days after the end of the month. A separate measure of the change in the total value of retail-level sales excluding automobiles is called core retail sales. The retail sales data set is generally expected to have a positive impact on digital assets if it is below expectations.

March 7 – U.S. Daylight Saving Time (DST) Shift; The US will switch to daylight saving time and clocks will move forward by 1 hour. As DST will be implemented in Europe on March 29, the opening and closing times of the US stock markets will be changed for almost the entire month of March compared to Europe.

Important Economic Calender Data

Click here to view the weekly Darkex Crypto and Economy Calendar.

Information

*The calendar is based on UTC (Coordinated Universal Time) time zone.

The calendar content on the relevant page is obtained from reliable data providers. The news in the calendar content, the date and time of the announcement of the news, possible changes in the previous, expectations and announced figures are provided by the data provider institutions.

Darkex cannot be held responsible for any changes arising from similar situations. You can also check the Darkex Calendar page or the economic calendar section in the daily reports for possible changes in the content and timing of data releases.

Legal Notice

The investment information, comments, and recommendations contained in this document do not constitute investment advisory services. Investment advisory services are provided by authorized institutions on a personal basis, taking into account the risk and return preferences of individuals. The comments and recommendations contained in this document are of a general nature. These recommendations may not be suitable for your financial situation and risk and return preferences. Therefore, making an investment decision based solely on the information contained in this document may not result in outcomes that align with your expectations.