Marktkompass

Geopolitical Agenda and More…

Last week, the global markets’ agenda was dominated by developments regarding tariffs, the US Federal Reserve’s monetary policy decisions and macro headlines. However, the main variable that dominated asset prices continued to be geopolitics. The level of conflict between Iran and Israel and the US stance on this issue came to the fore.

Although not far from historic highs, Bitcoin prices continue to be affected by global developments and the market’s risk appetite. Much has been made in recent days about whether the US will actually get involved in the escalating war between Iran and Israel. This is thought to exacerbate the already negative picture. At first, media reports suggested that Trump might attack Iran as soon as this weekend. However, the White House later clarified that the President would wait two weeks before deciding to attack Iran and that he would give a chance to sit down at the negotiating table, which he hoped would go well. This latest statement allowed the markets to breathe a little bit.

We believe that the reignited geopolitical risks in the Middle East will continue to occupy the markets in the medium term. Therefore, we felt the need to make a change in our guidance that we share in our daily bulletins this week. We expect digital assets to be flat in the medium term and bullish in the long term. Previously, in this investment horizon, we were also bullish in the medium term. However, as we mentioned, we see a solution to the Iran-Israel friction as unlikely in the short term. On the other hand, we think that it would not be correct to use the term “bearish” for the medium term, as we think that the vibrant demand for digital assets by institutional investors and the new US laws may cause possible pullbacks to be limited.

Geopolitical risks will again be on the agenda next week. Although Trump’s decision to give a two-week deadline for a decision on strikes brought some relief, the risks are still not over. On the other hand, markets will continue to monitor US macro indicators in the second half of the year to get an idea about the FED’s decisions that will determine the dose of global financial tightening. We will open a bear bracket on the most prominent ones.

FED Chair Powell’s Speech

At last week’s Federal Open Market Committee (FOMC) meeting, the US Federal Reserve left the policy rate unchanged as expected. What was noteworthy was the Committee’s downward revision in growth expectations and upward revision in inflation expectations. In addition, the FED seems to have kept its view that it may cut rates twice in the rest of the year and the Bank’s Chairman Powell made it clear that a wait-and-see strategy and any further changes at this time would be unwarranted.

Fed Chair Powell will make presentations to policymakers on Dienstag and Mittwoch. First, on Dienstag, he will speak before the House of Representatives Financial Services Committee in Washington DC about the Semi-Annual Monetary Policy Report and answer questions from the Committee members. On Mittwoch, he will repeat his presentation, this time before the Senate Committee on Banking, Housing and Urban Affairs. Of these, we can say that the speech on Dienstag is more important because the President will address both committees with the same text.

We do not expect Powell to change his stance as he did in the press conference following the last FOMC meeting. He will continue to say that the Fed will continue to wait for a better picture of the impact of the tariffs and that they will assess the economic repercussions of the developments in the Middle East. Apart from that, a surprise announcement could change the expectations (albeit unlikely) that the Bank could make two rate cuts by the end of the year. In such a case, we may see sharp changes in asset prices.

FED’s Favourite Inflation Indicator PCE

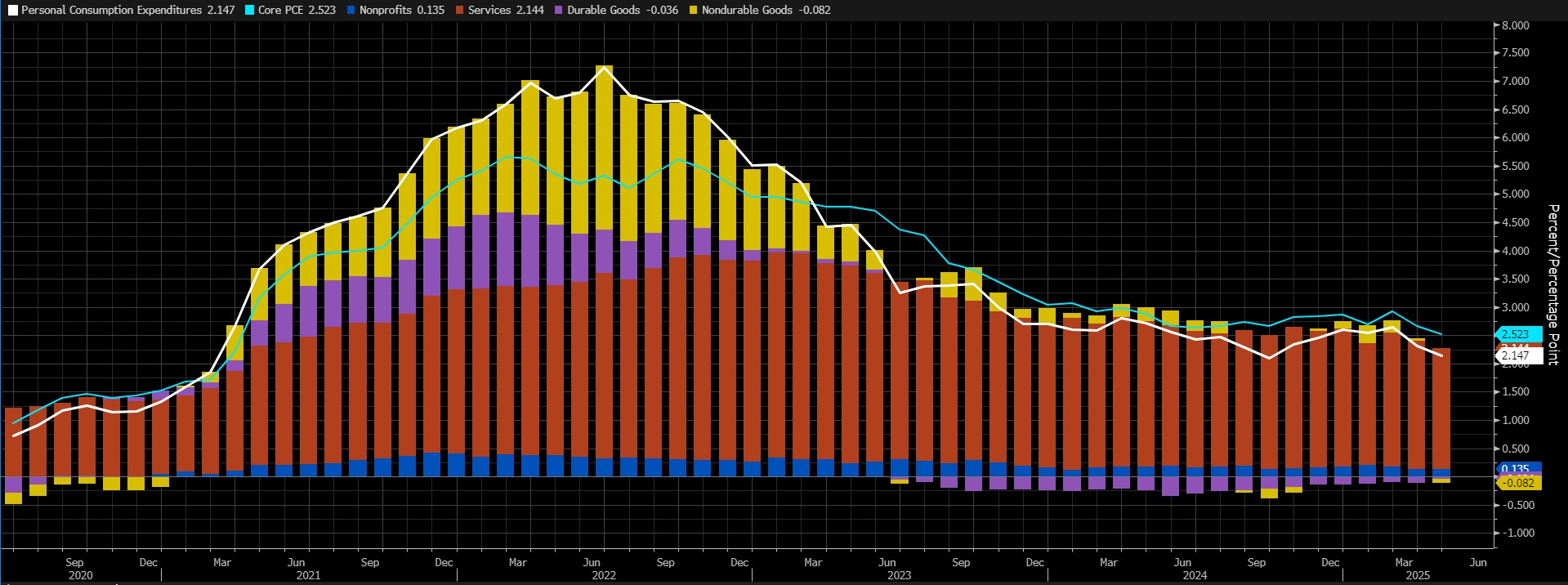

Markets will be closely watching the Personal Consumption Expenditures (PCE) data for Mai as they will try to get a clue as to which of the upcoming meetings of the Federal Open Market Committee (FOMC) will decide on a rate cut. This indicator is known as the preferred gauge for FOMC officials to monitor changes in inflation.

Quelle: Bloomberg

According to the latest data, core PCE increased by 0.1% mom in April. On an annual basis, core PCE increased by 2.5%. Thus, the index continued to decline for the second month after the 2.9% figure in Februar. We can say that we felt the Trump effect in this data as well. Our expectation is for an increase of around 0.25% in the core PCE data in Mai. This indicates a forecast that is slightly above market expectations.

Source: Darkex Research

A higher-than-expected data may support expectations that the FED will maintain its cautious stance on interest rate cuts, reducing risk appetite and putting pressure on digital assets. A lower-than-expected data may have the opposite effect and pave the way for value gains.

Other Macro Indicators to be Announced This Week

Flash Manufacturing PMI is a leading indicator of economic health. Businesses react quickly to market conditions and purchasing managers have perhaps the most up-to-date and relevant estimate of the company’s outlook for the economy. The Purchasing Managers’ Index (PMI) is a survey of nearly 800 purchasing managers that asks respondents to assess the relative level of business conditions, including employment, production, new orders, prices, supplier deliveries and inventories. Above 50.0 indicates that the sector is expanding, while below 50.0 indicates contraction. There are two versions of this report, Flash and Final, published about a week apart. The Flash version is released on a preliminary and monthly basis, approximately 3 weeks into the current month. A below-forecast reading is expected to produce a positive result for crypto assets.

CB Consumer Confidence It is the result of a survey of approximately 3,000 individual consumers asking respondents to assess the relative level of current and future economic conditions. It measures financial confidence as a leading indicator of consumer spending, which accounts for a large share of overall economic activity. It is published monthly, on the last Dienstag of the current month.

US Durable Goods Orders shows the change in the total value of new purchase orders placed with manufacturers for durable goods. This data is usually revised with the Factory Orders report released about a week later and “Durable Goods” are defined as products that last longer than 3 years, such as automobiles, computers, appliances and airplanes. It is a leading indicator of production and gives a preliminary indication of the vitality of the economy. Core Durable Goods Orders shows the change in the total value of new purchase orders placed with manufacturers for durable goods, excluding transportation items. This dataset has been shown to have complex effects on the value of digital assets.

Final GDP released quarterly, about 85 days after the quarter ends. There are 3 versions of GDP released a month apart – Advance, Preliminary, and Final. The Advance release is the earliest and thus tends to have the most impact. Final GDP generally does not have a significant impact on the markets and does not contain major revisions from the previous data.

*Allgemeine Informationen über Prognosen

In addition to the general market expectations, the forecasts shared in this report are based on econometric modeling tools developed by our research department. Different structures were considered for each indicator and appropriate regression models were constructed in line with data frequency (monthly/quarterly), leading economic indicators and data history.

The basic approach in all models is to interpret historical relationships based on data and to produce forecasts that have predictive power with current data. The performance of the models used is measured by standard metrics such as mean absolute error (MAE) and is regularly re-evaluated and improved. While the outputs of the models guide our economic analysis, they also aim to contribute to strategic decision-making processes for our investors and business partners. Data is sourced directly from the FRED (Federal Reserve Economic Data) platform in an up-to-date and automated manner, so that every forecast is based on the latest economic data. As the research department, we are also working on artificial intelligence-based modeling methods (e.g. Random Forest, Lasso/Ridge regressions, ensemble models) in order to improve forecast accuracy and react more sensitively to market dynamics. The macroeconomic context should be taken into account in the interpretation of model outputs, and it should be kept in mind that there may be deviations in forecast performance due to economic shocks, policy changes and unforeseen external factors. With this monthly updated working set, we aim to provide a more transparent, consistent and data-based basis for monitoring the macroeconomic outlook and strengthening decision support processes.

Research Department Current Studies

Monatlicher Bericht zur Kryptomarktanalyse

Wöchentliche BTC Onchain-Analyse

Wöchentliche ETH Onchain-Analyse

Robinhood’s RWA Move: A New Financial Era?

Stars of Social Media: 5 Altcoins Shining in the Recent Bitcoin Rally

Effects of FED’s Interest Rate Decisions on Cryptocurrency Markets

Bitcoin and BlackRock: Decentralization at Risk?

Klicken Sie hier für alle unsere anderen Market Pulse Berichte.

Important Economic Calendar Data

Klicken Sie hier um den wöchentlichen Darkex Krypto- und Wirtschaftskalender zu sehen.

Informationen

*Der Kalender basiert auf der Zeitzone UTC (Coordinated Universal Time).

Der Kalenderinhalt auf der entsprechenden Seite wird von zuverlässigen Datenanbietern bezogen. Die Nachrichten in den Kalenderinhalten, das Datum und die Uhrzeit der Bekanntgabe der Nachrichten, mögliche Änderungen der bisherigen, erwarteten und angekündigten Zahlen werden von den Datenanbietern Institutionen gemacht.

Darkex kann nicht für mögliche Änderungen, die sich aus ähnlichen Situationen ergeben, verantwortlich gemacht werden. Sie können auch die Darkex-Kalender-Seite oder den Wirtschaftskalender in den Tagesberichten auf mögliche Änderungen von Inhalt und Zeitpunkt der Datenveröffentlichungen überprüfen.

Rechtlicher Hinweis

Die in diesem Dokument enthaltenen Anlageinformationen, Kommentare und Empfehlungen stellen keine Anlageberatungsdienste dar. Die Anlageberatung wird von zugelassenen Instituten auf persönlicher Basis unter Berücksichtigung der Risiko- und Ertragspräferenzen des Einzelnen durchgeführt. Die in diesem Dokument enthaltenen Kommentare und Empfehlungen sind allgemeiner Art. Diese Empfehlungen sind möglicherweise nicht für Ihre finanzielle Situation und Ihre Risiko- und Renditepräferenzen geeignet. Eine Anlageentscheidung, die ausschließlich auf der Grundlage der in diesem Dokument enthaltenen Informationen getroffen wird, kann daher möglicherweise nicht zu Ergebnissen führen, die mit Ihren Erwartungen übereinstimmen.