BRÚJULA DE MERCADO

Los activos digitales están atravesando otra semana complicada, al igual que los mercados tradicionales. Las acciones y declaraciones de Trump sobre los aranceles, así como su decisión de llevar delegaciones a Riad para mantener conversaciones de paz con Rusia sobre Ucrania, pasando por alto a Europa e incluso a la propia Ucrania, han recibido una amplia cobertura. El nuevo presidente estadounidense sigue gobernando de forma impredecible. El continente europeo no está muy contento con esta situación. Alemania, la mayor economía del continente, acude a las urnas este domingo. Aunque se espera que el antiinmigrante Friedrich Merz sea el próximo primer ministro de Alemania, queda por ver cómo afrontará la amenaza de Trump de imponer aranceles a las importaciones si resulta elegido. Los resultados de las elecciones serán importantes no sólo para Alemania, sino para toda Europa.

La evolución de la economía estadounidense sigue impulsando los precios de todos los activos financieros sin excepción. Aparte del estilo de gobierno de Trump, siguen siendo importantes la salud de la economía estadounidense y las expectativas sobre cómo la Reserva Federal de EE.UU. (FED) configurará su política monetaria frente a él. Es probable que la agenda macroeconómica, que pasó a un segundo plano la semana pasada debido a los aranceles y las conversaciones en Riad, se siga más de cerca esta semana con datos de crecimiento e inflación como el índice de precios PCE. Por lo tanto, nos parece oportuno abrir un paréntesis aparte para estos indicadores que pueden afectar a las expectativas del mercado y a la evolución de los precios.

El problema del crecimiento económico en EE.UU.

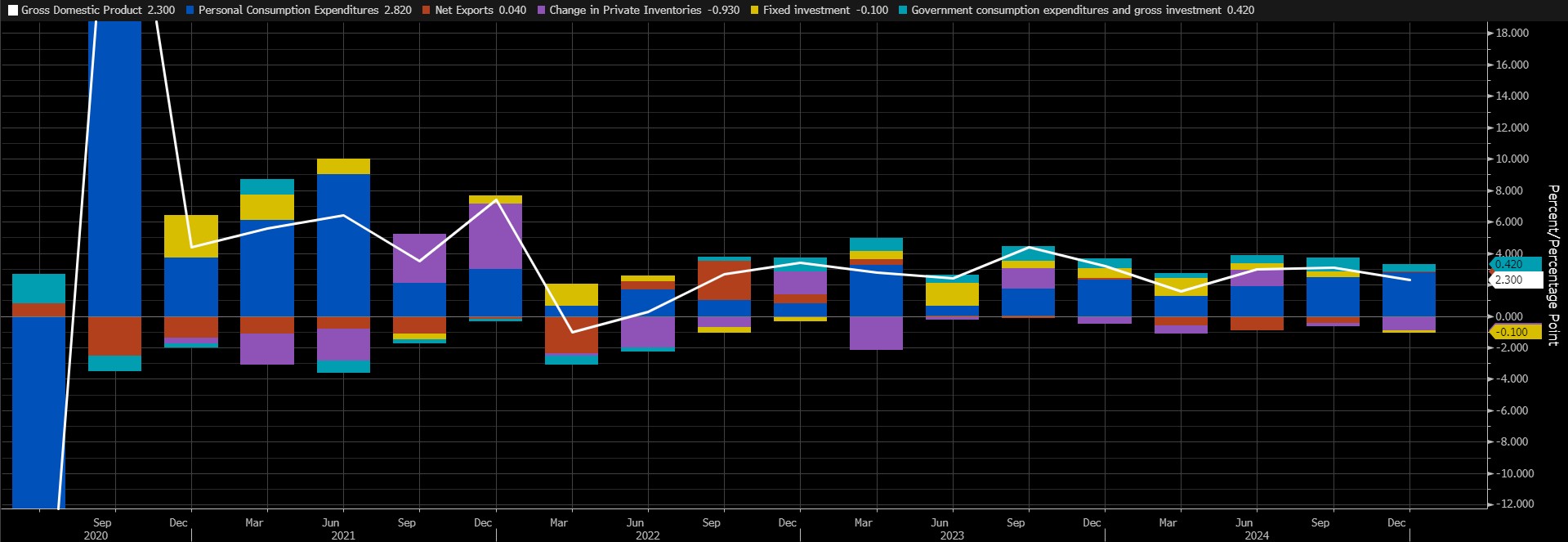

La mayor economía del mundo creció a una tasa anualizada del 2,3% en el cuarto trimestre de 2024, el ritmo más lento en tres trimestres y un ritmo de crecimiento más conservador que el 3,1% del tercer trimestre y el 2,6% previsto. El nuevo dato que se publicará el jueves será la segunda estimación de la Oficina de Análisis Económicos para el último trimestre del año pasado. Según datos de Bloomberg, no se esperan cambios respecto a la primera cifra publicada del 2,3%.

Fuente: Bloomberg

En los primeros datos publicados para este trimestre, los gastos de consumo personal, que son el motor de la economía estadounidense, fueron de nuevo los que más contribuyeron al crecimiento económico. No esperamos un cambio significativo en este sentido. Tampoco creemos que veamos una desviación significativa de la previsión mediana del 2,3%. Aunque es justo decir que los datos de crecimiento del primer trimestre serán más importantes en los próximos meses, cabe señalar que una revisión potencialmente importante de los datos del PIB que se publicarán esta semana podría afectar al comportamiento de los precios.

En este momento, existen dos escenarios posibles. Creemos que un dato de crecimiento del PIB ligeramente por encima o por debajo de las previsiones impulsará las expectativas sobre la política monetaria de la Reserva Federal estadounidense (FED). En este contexto, un dato del PIB ligeramente por debajo de las previsiones (como un 2,2%-2,1%) puede aumentar el apetito por el riesgo en los mercados al apoyar las expectativas de que la FED se atreverá con un nuevo recorte de los tipos de interés, lo que puede allanar el camino para la apreciación de los activos digitales. Un dato ligeramente superior al esperado (2,4%-2,5%) podría apoyar la percepción de que la FED esperará más tiempo para recortar los tipos de forma precipitada. En tal caso, podrían observarse pérdidas en las clases de activos consideradas relativamente más arriesgadas. En el segundo escenario, hay que considerar el caso de que el PIB difiera significativamente de las expectativas. Una lectura sorpresa del 2% o inferior podría desencadenar la preocupación de que el crecimiento de la mayor economía del mundo es realmente problemático. Aunque esto probablemente acercaría a la Reserva Federal a recortar los tipos de interés, la preocupación por el crecimiento (y quizás por la recesión) podría provocar un cambio significativo en el apetito por el riesgo, lo que podría ejercer presión vendedora sobre los instrumentos financieros, incluidos los activos digitales. Merece la pena subrayar que un dato significativamente positivo, aunque pensamos que no tendrá tanto impacto como los malos precios, puede aumentar el apetito por el riesgo y proporcionar una base para las subidas.

En resumen, los datos de crecimiento de EE.UU. serán un dato importante para todos los mercados. Sin embargo, su importancia para los mercados financieros puede reducirse a lo lejos de las expectativas que veamos una cifra que sorprenda a los mercados. Aunque creemos que es poco probable que veamos una serie de datos que afecten al comportamiento de los precios y provoquen una sacudida, no descartamos un escenario en el que podríamos ver fuertes cambios en los precios si vemos datos sorpresa.

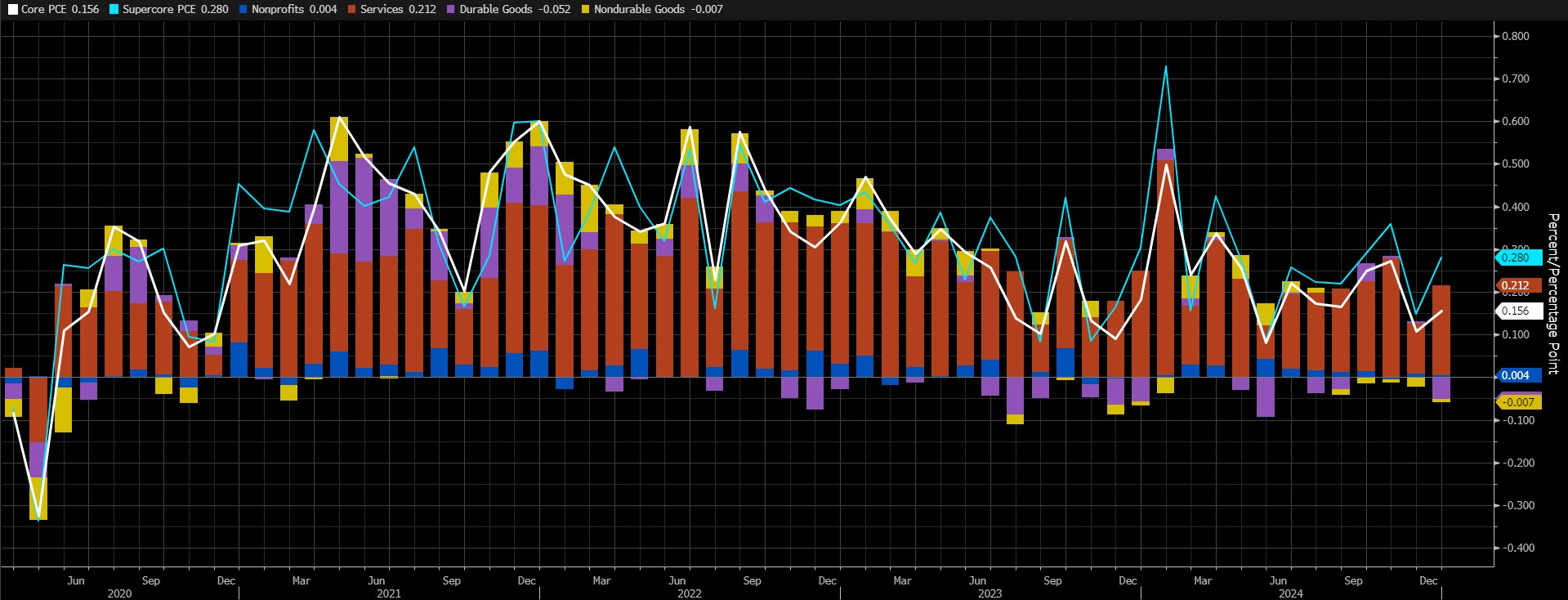

Indicador de inflación de la FED: PCE

El discurso del presidente de la Reserva Federal estadounidense, Powell, en el simposio de Jackson Hole del año pasado provocó un cambio significativo en la ecuación. Powell desplazó el foco de atención de la inflación a la fortaleza del mercado laboral y lanzó mensajes de que la FED daría ahora más importancia a la fortaleza del mercado laboral en sus decisiones. O al menos así es como los mercados interpretaron estas declaraciones. Los últimos meses han demostrado que éste puede no ser el enfoque adecuado.

En enero, el índice de precios al consumo (IPC) se situó en el 3% sobre una base anualizada. En septiembre, con una lectura del 2,4%, apuntaba al menor aumento de la inflación desde febrero de 2021. Así pues, este IPC de septiembre apunta a mayores incrementos. En este sentido, podemos decir que la FED ha seguido un camino criticable. Por otro lado, el índice de precios PCE subyacente (anualizado), que la FED considera el seguimiento de los cambios en la inflación, se ha mantenido sin cambios (2,8%) durante los tres últimos meses (octubre-noviembre-diciembre). Los datos mensuales de este indicador habían apuntado a un aumento del 0,2% en diciembre. Creemos que este es el dato que será importante para los mercados el viernes.

Fuente: Bloomberg

Algunas partidas del índice de precios a la producción (IPP), que constituyen algunos componentes de los datos del PCE, llamaron la atención, ya que los datos del IPP publicados el 13 de febrero se situaron por encima de las previsiones. Sin embargo, la variación de las ventas al por menor del mismo mes (datos de enero), que también se calcula por variación mensual, indicó que el gasto en el país disminuyó más rápido de lo previsto. En otras palabras, podemos decir que observamos dos macrodatos en la semana anterior que dificultaron la previsión del PCE.

Según Bloomberg, se espera que los datos del índice de precios PCE subyacente (m/m) apunten a un aumento del 0,3% en enero. Una previsión superior a la media podría respaldar las expectativas de que la Fed mantendrá su postura cautelosa en cuanto a los recortes de tipos, lo que reduciría el apetito por el riesgo y pesaría sobre los activos digitales. Una lectura inferior a la prevista, por el contrario, podría tener el efecto contrario y allanar el camino a las ganancias de valor.

DEPARTAMENTO DE INVESTIGACIÓN DARKEX ESTUDIOS ACTUALES

Análisis semanal de BTC Onchain - 19 de febrero

Análisis semanal de ETH Onchain - 19 de febrero

Alta correlación entre Bitcoin y el índice Russell 2000: Causas y consecuencias

La revolución de los fondos de activos digitales: El proceso de los ETF de altcoin

Aranceles a Canadá y México bajo los aranceles de Donald Trump

Blackrock De Fondo Específico Rwa y Rendimientos de Ondo, Maple, Pendle

Pulse aquí para consultar el resto de nuestros informes Market Pulse.

DATOS IMPORTANTES DEL CALENDARIO ECONÓMICO

Pulse aquí para ver el calendario semanal de cripto y economía de Darkex.

INFORMACIÓN:

*El calendario se basa en la zona horaria UTC (Tiempo Universal Coordinado).

El contenido del calendario en la página correspondiente se obtiene de proveedores de datos fiables. Las noticias del contenido del calendario, la fecha y hora del anuncio de la noticia, los posibles cambios en las cifras anteriores, las expectativas y las cifras anunciadas son realizadas por las instituciones proveedoras de datos.

Darkex no se hace responsable de posibles cambios derivados de situaciones similares. También puede consultar la página del calendario Darkex o la sección del calendario económico en los informes diarios para conocer los posibles cambios en el contenido y el calendario de publicación de los datos.

AVISO LEGAL

La información sobre inversiones, los comentarios y las recomendaciones contenidas en este documento no constituyen servicios de asesoramiento en materia de inversiones. Los servicios de asesoramiento en materia de inversión son prestados por instituciones autorizadas a título personal, teniendo en cuenta las preferencias de riesgo y rentabilidad de los particulares. Los comentarios y recomendaciones contenidos en este documento son de tipo general. Estas recomendaciones pueden no ser adecuadas para su situación financiera y sus preferencias de riesgo y rentabilidad. Por lo tanto, tomar una decisión de inversión basándose únicamente en la información contenida en este documento puede no dar lugar a resultados acordes con sus expectativas.